Report

Q2 2025 Industry Insights

South Africa’s Credit Market Expanded During Q2 2025 Amid Eased Interest Rates and Shifting Consumer Risk

Q2 2025 Report highlights include:

- Millennial consumers drove significant new credit card growth, although new card limits dropped significantly

- Vehicle asset finance growth trend continued, with more than two thirds of loans originated by Gen Z and Millennial consumers

- Eased interest rates drove year-over-year growth in home loan originations, although affordability pressures may be impacting performance

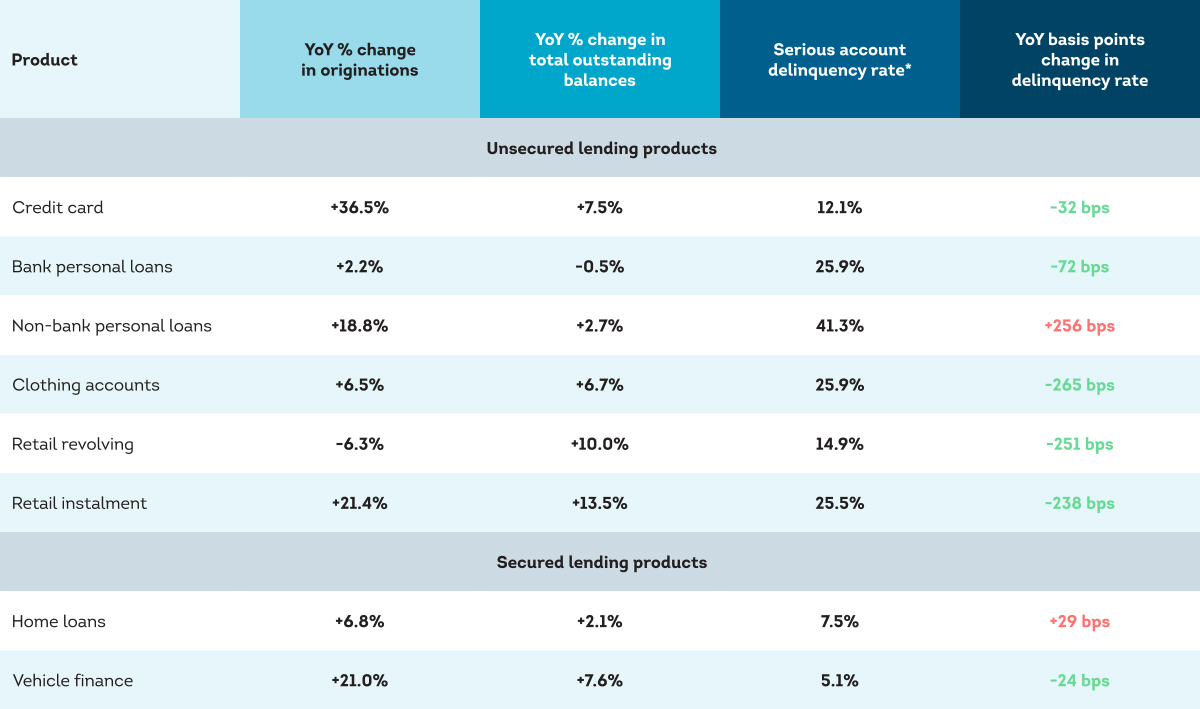

South Africans responded to a more favourable interest rate environment during Q2 2025, leading to increased new account originations across most consumer credit products, particularly for credit cards and vehicle finance. Home loan activity also showed signs of recovery, as consumers felt more confident in committing to longer-term credit obligations. Retail revolving loans were the exception, with origination volumes declining despite growth in balances.

These are some of the findings of TransUnion’s Q2 2025 South Africa Industry Insights Report, which also found that South Africans were managing their credit better, as delinquencies improved across most consumer credit products during the quarter.

Q2 2025 Metrics for Consumer Credit Products

"For vehicle finance lenders, the rise in originations alongside modest growth in loan amounts suggests an opportunity to support demand while maintaining portfolio discipline. The improvement in delinquency rates is encouraging, but ongoing monitoring will be essential as economic recovery remains uneven. Vehicle finance lenders may benefit from refining pricing models, reassessing vehicle segmentation strategies, and balancing growth with prudent risk management."

Ayesha Hatea, director of research and consulting at TransUnion

About the South Africa Industry Insights Report

TransUnion’s quarterly South Africa Industry Insights Report provides in-depth, statistical information drawn from its national consumer credit database, aggregated across virtually every active credit file on record. Each file contains hundreds of credit variables that illustrate consumer credit usage and performance. Entities across industries can subscribe to and leverage the Industry Insights Report to analyse market dynamics throughout an entire business cycle, helping them understand consumer behaviour over time.

The report looks at major consumer lending categories: credit cards, personal loans, home loans, vehicle and asset finance (VAF), and clothing, focusing primarily on three dimensions across these categories: originations (new accounts opened), balances (outstanding total and average lending balances) and delinquencies (accounts in payment arrears).

GET THE REPORT

The submission has failed.